Ujjwal Thakur

Last Updated on 25th June 2026

Ujjwal Thakur

Last Updated on 25th June 2026

If you are planning to apply for a home loan in the next year or two, your CIBIL score may matter more than ever.

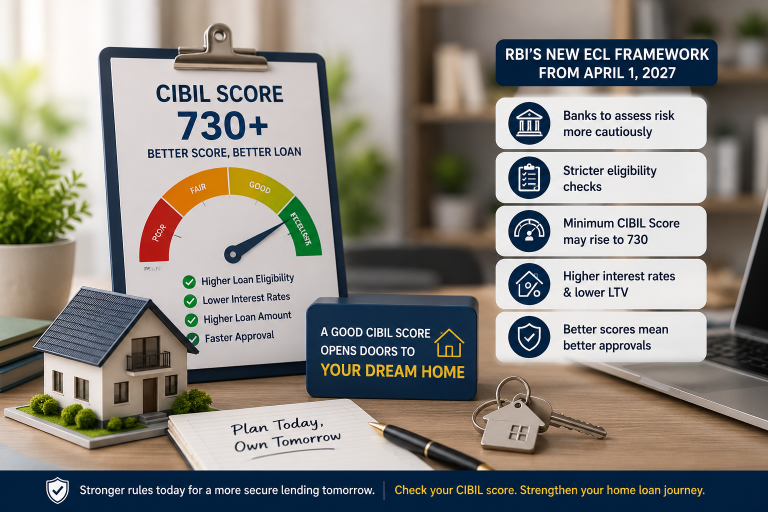

The Reserve Bank of India (RBI) is preparing to introduce the Expected Credit Loan (ECL) framework from April 1, 2027, which may lead to banks assessing home loan applicants more cautiously. This could mean stricter home loan eligibility checks, scrutiny of repayment history, and the minimum CIBIL score requirement might rise to 730.

Read the blog further to understand how the new rule could impact your home loan application, the minimum CIBIL required, and existing loans.

Millions of home loan seekers are wondering whether the RBI’s new change could affect their home loan applications. As per the suggested changes, banks could change the prerequisites for home loan applications and sanctions to avoid Non-Performing Assets (NPAs). Unlike earlier, the new rules suggest that banks should predict losses on bad loans and set aside funds for the RBI. Due to this, banks are likely to increase the interest rate, CIBIL score eligibility, and loan-to-value ratio to minimize the loss and filter out the potential loan defaulters.

So yes, RBI’s new loan could affect your home loan application and CIBIL score criteria.

As per the new ECL norms, the minimum CIBIL required to secure a home loan is going to be beyond 730. Unlike earlier, a credit score of 700-720 may not guarantee you a home loan. Banks are likely to check your credit history more strictly and may not offer you a home loan if they find some irregularities in your repayment history. Similarly, if you have a 730+ CIBIL score, the chances of securing a home loan are higher at better interest rates. The new norms also direct banks to scrutinize your CIBIL score and credit history even after loan sanctioning.

| CIBIL Score | Impact of RBI’s ECL Framework on Home Loan |

|---|---|

| 780+ | Better interest rates, faster loan approval, and higher home loan eligibility. |

| 730-799 | Standard interest rates, stricter financial scrutiny, and possible impact on the sanctioned loan amount. |

| Below 730 | Higher interest rates, increased chances of loan rejection, and a larger down payment may be required. |

| Below 700 | Very low chances of home loan approval from most banks. |

The RBI’s new guidelines may also impact the way banks calculate your home loan interest. Till FY28, the home loan continues to follow a one-size-fits-all interest method. However, the new changes may inspire a lot of changes. Earlier, banks used to offer one home loan interest rate to all, but to minimize the risk of financial loss in loan defaults, banks may charge higher interest rates to those with low CIBIL scores.

The percentage of the property cost that banks lend to home loan borrowers is called the Loan-to-Value (LTV) Ratio. When the new ECL norms are in full effect, the banks may give a lower LTV ratio.

For example, a bank sanctions 85-90% LTV when you take a home loan as per the current norms. So if your property costs 50 lac, banks give a home loan amount of 35 lac to 40 lac. After the ECL framework, banks may give you a lower LTV based on your credit score, income, and other factors.

Expected Credit Loss (ECL) Framework is a future-oriented loan provisioning model that enables banks to minimize the risk of Non-Performing Assets (NPAs)/loan defaults before the loan goes bad. Through this model, RBI directs banks to analyze and set apart some provision funds before the loss occurs. Currently, all the banks use the Incurred Loss Model to assess the bad performing loan and take action against them. Unlike ECL, the Incurred Loss Model is less predictive and more reactionary in its strategy.

Hence, the RBI directs all the banks to adopt the new model to ensure they can predict and classify the loss before they occur and take cautionary measures.

Secured loans are collateral-based, and unsecured loans are free from any collateral. After the implementation of new frameworks, both these loan types may face some effects. The effects on secured loans like car loans and home loans may be slightly less, as banks can recover the loan amount by seizing the assets. Whereas unsecured loans may go through drastic changes as they are collateral-free loans and are risk-heavy.

The provision amount on home loans could be 0.25%-0.50% of the total amount based on the loan repayment history, credit history, loan default type, and employment stability. Unlike secured loans, the provision amount could go up to 1-3% based on various factors.

After the implementation of the new RBI norms for home loans, freelancers and gig workers may face a bigger risk of home loan application rejection. Since the income is likely to be unstable and irregular for them, banks may see them as potential loan defaulters.

Some of the things that you can do to minimize the bad effects of ECL on your home loan application are as follows:

The RBI’s new ECL framework could change the way India lends and borrows. That’s why we advise you to increase your financial literacy to enhance your financial journey. Whenever you apply for a home loan, you should seek all the information you can get beforehand. And at BASIC, we help you with all the latest news and trends on home loans, finding the best lender, and securing the loan. We are India’s leading home loan advisor who can help you negate the effects of ECL norms. Connect with us and take your home loan journey forward.

Get a loan in under 5 mins