BASIC TEAM

Last Updated on 13th March 2026

BASIC TEAM

Last Updated on 13th March 2026

If you wish to buy an affordable home in Maharashtra, the MHADA lottery is the perfect opportunity for you. It is a lottery system organized by the Maharashtra Housing and Area Development Authority (MHADA) and helps thousands of people get their dream homes at a reasonable price every year. Read the blog to know the eligibility criteria and application process for the MHADA Lottery 2025. Whether you’re applying for the first time or looking to better understand the process, this beginner-friendly guide is here to simplify everything and help you take the right steps toward homeownership.

Table of Contents

Paying off a home loan before its scheduled end date is known as home loan foreclosure. Many people choose the preclosure of home loans for various reasons.

One of these reasons could be to secure the lowest interest rate for a housing loan from another bank. This is where the concept of refinancing comes into play. When you refinance, the new bank pays off your existing loan, and you begin a new loan with better terms. This is essentially a form of foreclosure since the original loan is being paid off before its scheduled end date.

Refinancing is an attractive option for many borrowers because it can lead to significant savings over the life of the loan. For example, if the new bank offers a lower interest rate, the borrower could end up paying less in interest over the life of the loan, even when taking into account the costs of refinancing. This is why some borrowers might choose to foreclose their original loan and start a new one with a different bank.

However, it’s important to note that foreclosure and refinancing are not the same thing, and each comes with its considerations and potential costs. For example, some banks might charge a penalty for foreclosure, and there are also costs associated with refinancing, such as application fees and closing costs. Therefore, it’s important for borrowers to carefully consider their options and consult with a financial advisor before deciding to foreclose or refinance their home loan.

Importantly, one significant advantage of home loan foreclosure is reducing the interest burden and the overall cost of the property. In India, where the average home loan tenure is around 8 years, opting for prepayment can be beneficial. This approach is often taken when individuals receive an annual bonus or when their existing investments mature

Suggested read: Home Loan With Low Credit Score

Pre-closing a home loan, which means paying off your mortgage before the agreed term ends, can sound like a great idea for financial freedom. However, it comes with its own set of demerits to consider:

|

Lender |

Individual Borrowers |

Non-individual Borrowers |

|

Nil to 2% |

Nil to 2% |

|

|

Nil to 3% |

Nil to 3% |

|

|

Dhanlaxmi Bank |

Nil |

As per the terms of the bank |

|

Nil for floating rates 4% of outstanding principal – for fixed rates |

Nil for floating rates 4% of outstanding principal – for fixed rates |

|

|

Nil to 4% |

Nil to 4% |

|

|

Nil to 2% |

Nil to 2% |

|

|

Nil to 3% |

Nil to 3% |

|

|

Oriental Bank of Commerce |

Nil |

Nil |

|

Axis Bank |

Nil |

Nil |

|

Aditya Birla Housing Finance Ltd. |

Nil |

2% for outstanding principal |

Suggested read: Best home loan bank in India

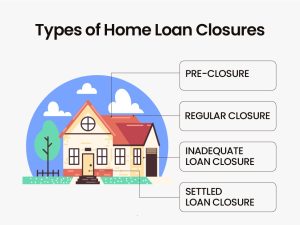

There are various types of home loan closures, such as:

While foreclosure can save on interest, evaluating the financial implications and how they may affect your daily expenses is essential.

Here are the essential documents you should collect after you’ve paid off your home loan to ensure everything is squared away:

By following these steps, you can confidently navigate the home loan pre-closure process

Suggested read: Pre-payment of Home Loan

It’s important to be aware that not all home loan providers enable online prepayment facilities. In such cases, borrowers may need to physically visit the bank or authorize a representative to make the prepayment.

Fortunately, there are typically no restrictions on authorizing someone else to carry out the prepayment, as long as the lending institution’s prepayment rules are followed.

Before proceeding with foreclosure, individuals should carefully assess any prepayment charges imposed by the bank. In some instances, these charges may outweigh the interest savings, making it less financially beneficial to pre-close the loan.

Banks may charge a prepayment penalty to discourage early loan repayment and protect their interest income. However, if your loan has a floating interest rate, the RBI prohibits banks from levying such penalties. For fixed-rate loans, the penalty can be up to three percent.

If you prepay after six months, you can prepay up to 25% without penalties, but beyond that, a fee may apply.

Before prepaying, consider the impact on tax benefits, as prepayment may affect deductions on interest payments (up to Rs 2 lakh under section 24(b)) and principal repayment (up to Rs 1.5 lakh under section 80C).

Additionally, it’s essential to prioritize prepayment in the early years to save more on interest. If you have other high-interest-rate loans, paying them off first could be more beneficial.

Indiabulls, Sundaram Home Finance Limited, Axis Bank, DBS Bank, Gruh Finance Limited, Oriental Bank of Commerce, Canara Bank, Kotak Mahindra Bank, and Jammu & Kashmir Bank – All offer nil prepayment charges for both individual and non-individual borrowers.

In conclusion, understanding home loan foreclosure charges is essential for any borrower. Preclosing a home loan can provide various benefits, including saving on interest and reducing the overall cost of the property. However, borrowers must carefully weigh the pros and cons, considering factors such as financial stability, home loan tax benefits, and future monetary requirements. If opting for preclosure, ensuring a smooth process by following necessary guidelines and evaluating prepayment charges is crucial. Ultimately, making an informed decision will help borrowers navigate this financial aspect with confidence and achieve their homeownership goals effectively.

Yes, banks can levy foreclosure charges on home loans, but as per RBI guidelines, no charges are to be levied on floating-rate term loans sanctioned to individual borrowers.

RBI guidelines state that banks will not levy foreclosure charges or prepayment penalties on home loans on a floating interest rate basis.

You can avoid foreclosure charges by choosing a loan with a floating interest rate, as per RBI guidelines, or by negotiating with your bank.

Foreclosure of a home loan can save on the interest that would have been paid during the remaining loan tenure, but it doesn’t reduce the interest rate.

The foreclosure amount is calculated as the sum of the outstanding principal amount, accrued interest, and any applicable charges.

Benefits include saving on interest payments, improving credit scores, and reducing financial burdens.

Foreclosure refers to repaying the entire loan amount in one go, while prepayment pays off part of the loan in advance.

Yes, prepayment of home loans can reduce EMIs as it reduces the outstanding principal amount, leading to a smaller loan balance and, therefore, potentially lower monthly EMIs.

Get a loan in under 5 mins