Last Updated on 17th October 2024

Getting home loan is very BASIC now

Get a loan in under 5 mins

Last Updated on 17th October 2024

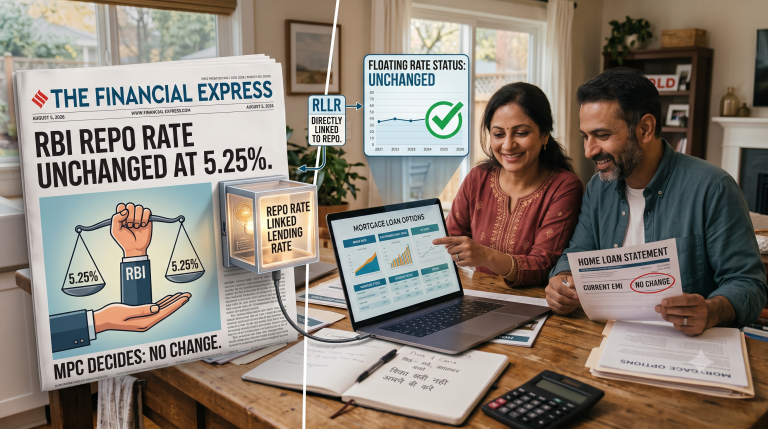

In a significant decision for home loan borrowers, the Reserve Bank of India (RBI) has once again kept the repo rate unchanged at 6.5% during the recent meeting of the Monetary Policy Committee (MPC). This marks the 10th consecutive time that the central bank has maintained the status quo, providing much-needed stability for borrowers as home loan interest rates and equated monthly installments (EMIs) remain unchanged.

By holding the repo rate steady, the RBI aims to strike a delicate balance between controlling inflation and fostering economic growth. Home loan borrowers, especially those with floating-rate loans tied to the repo rate, will continue to benefit from predictable EMIs, aiding in their financial planning.

The Reserve Bank of India’s (RBI) three-day Monetary Policy Committee (MPC) meeting took place from October 7 to 9. This meeting was significant as it marked the first gathering of the six-member MPC since the replacement of half its members the previous week.

Since the adoption of the external benchmark system in October 2019, most banks have linked their floating-rate retail loans, including home loans, to the repo rate. This means any changes in the repo rate are directly reflected in home loan interest rates. While a rate hike typically increases borrowers’ interest burdens, a stable or lower repo rate ensures that home loan EMIs remain affordable.

The decision to keep the repo rate unchanged will likely keep home loan interest rates stable in the short term. However, economists are optimistic about a possible rate cut from December onwards, driven by an improving inflation outlook and the start of a global monetary easing cycle. This could bring relief to existing home loan borrowers and potentially reduce their interest payments.

The RBI’s neutral stance suggests that it could go either way in future decisions. With inflation hovering near the medium-term target of 4% and the global monetary easing cycle gaining momentum, economists expect a rate cut as early as December. A reduction in the repo rate could bring much-needed relief to home loan borrowers, particularly those with large outstanding amounts.

For example, a 25 bps (basis points) rate cut over three tranches could lower interest rates from 9.25% to 8.5%, potentially reversing the burden of previous rate hikes and reducing the total interest payable on a home loan.

Earlier in October, the Indian government appointed three new external members to the MPC, a routine process in which the central government nominates and appoints these members. The newly appointed members are Saugata Bhattacharya, an economist; Dr. Nagesh Kumar, Director and Chief Executive at the Institute for Studies in Industrial Development; and Professor Ram Singh, Director of the Delhi School of Economics, University of Delhi.

These new members joined RBI Governor and MPC Chairperson Shaktikanta Das, Executive Director Rajiv Ranjan, and Deputy Governor Michael Debabrata Patra on the panel. Bhattacharya, Kumar, and Singh replaced former external members Shashanka Bhide, Ashima Goyal, and Jayanth R. Varma.

While home loan EMIs remain steady for now, borrowers can still take proactive steps to reduce their overall interest burden. One such strategy is making partial prepayments toward the principal amount. By channeling extra savings or portions of bonuses towards prepayments, borrowers can significantly reduce their loan tenure and save substantial amounts in interest over time.

Even modest prepayments can have a profound impact on the total interest paid, helping borrowers pay off their loans faster and with less financial strain. Making this a yearly habit, especially during times of stable or high-interest rates, can provide long-term financial benefits.

New home loan borrowers should pay close attention to the spread applied by different banks over the repo rate. Banks like HDFC and SBI have recently increased home loan rates for new customers, despite no changes in the repo rate. For instance, the lowest home loan rate at HDFC Bank increased from 8.35% in January to 8.75%, highlighting the importance of finding a lender that offers a competitive spread.

Borrowers should explore options from various lenders and compare interest rates to secure the most favorable terms. Opting for a lender with a narrow spread can help reduce the overall interest burden and ensure that EMIs remain manageable throughout the loan tenure.

In the current scenario, existing home loan borrowers tied to older benchmarks like the marginal cost of funds-based lending rate (MCLR) or the base rate should consider switching lenders. This is especially true if they are paying higher interest rates compared to newer loans linked to the repo rate. Many banks are offering loans starting at 8.35%, which could significantly reduce the interest burden for borrowers willing to make the switch.

Additionally, borrowers should explore negotiating with their current lenders to secure lower rates. While banks may not have a formal conversion process, they are often willing to negotiate rates, particularly if customers indicate plans to switch to a different lender.

Conclusion: Stability for Now, but Potential Savings Ahead

For home loan borrowers, the RBI’s decision to keep the repo rate unchanged offers immediate stability, with EMIs and interest rates remaining constant. However, with the possibility of a repo rate cut in the near future, borrowers should stay informed and consider strategic moves such as partial prepayments and lender switches to optimize their financial position.

As the economic landscape evolves, keeping a close eye on rate trends and exploring opportunities for savings can help borrowers reduce their home loan burdens and achieve long-term financial stability.

Get a loan in under 5 mins